January 25, 2017

Dear Valued Investor:

I hope that you have enjoyed spending time with loved ones during this holiday season. This time of year often presents an opportunity for some additional rest and relaxation, but there is always the possibility for activity in the markets—or as was the case last week, the government. Friday, December 22, 2017, President Trump signed the 2017 Tax Cuts and Jobs Act into law. Although the depth of detail of this new law may be intimidating, on balance, its passage may provide firmer footing for investors as we begin a new year.

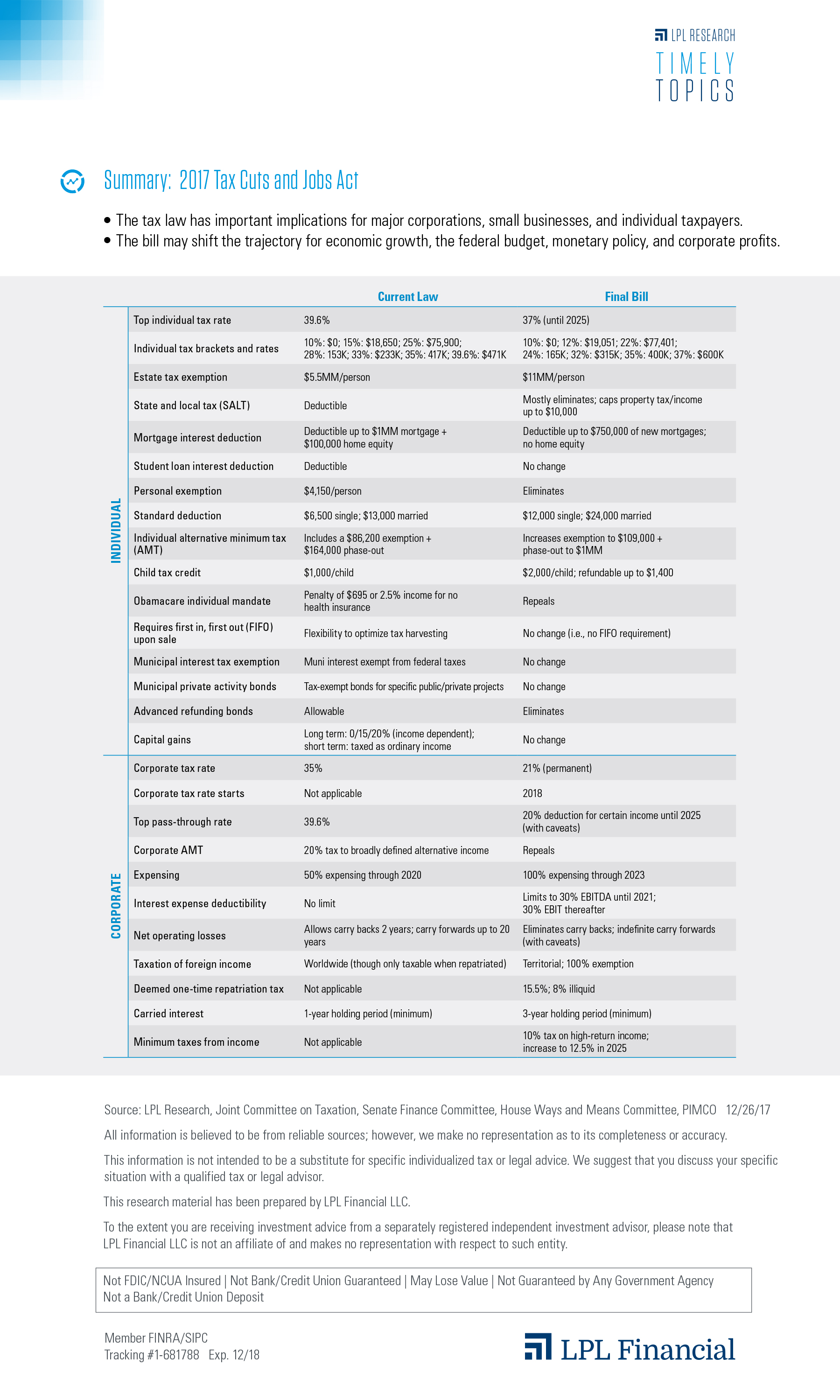

The $1.5 trillion tax cut is a complex, 1,000-page law intended to spur economic activity through a reduction in both individual and corporate tax rates, and simplify the tax code by eliminating or trimming a variety of deductions and exemptions. At a high-level overview:

- The Joint Committee on Taxation suggests the estimated total cost over 10 years will be just over $1 trillion, with the offset of $500 billion in added revenue from an estimated economic growth impact of +0.7% per year over the next 10 years.

- The estimated net tax cuts for individuals total approximately $1.15 trillion, or about 77% of the package, a greater focus on individual tax cuts than the original House bill.

- The estimated net tax cuts for U.S. corporations total around $330 billion, or 23% of the overall package.

The new tax law has important implications for major corporations, small businesses, and individual taxpayers, and is designed to shift the trajectory for economic growth, the federal budget, monetary policy, and perhaps most critically for investors—corporate profits.

There are legitimate concerns that the new law could increase the potential for higher inflation and weigh on the deficit. Yet U.S. consumers may be poised to reap approximately $100 billion in 2018 and $200 billion in 2019 thanks to the individual tax cuts. Meanwhile, U.S. corporations can potentially boost investment from a combination of lower taxes, repatriated profits, and immediate expensing, further supporting economic growth. It appears initially that Telecom and industrials are poised for the greatest potential benefit, although this is not a recommendation for either assets class.

Perhaps the biggest immediate takeaway for investors is that the accelerated timeline to pass the law has decreased uncertainty. As a result, individuals and businesses have the opportunity to begin planning around the changes and pulling forward the new law’s impact.

With the new tax law in play, Maverick Wealth Management is upgrading its projections for 2018 U.S. economic growth to 2.75% from its original forecast of 2.5%, raising estimates for corporate profits, and consequently increasing its projection for the S&P 500 Index’s price target to a range of 2825 by year-end.* This upgraded S&P 500 target increases Maverick Wealth Management’s broad return expectations for 2018 at approximately 8-10% including dividends, while the we still maintains a cautious bond market view, due to the greater risk of rising interest rates.

We are cautious that any number of events could spur a bear market sooner than later. In fact, after the tax bill passed Morgan Stanley (who posted Wall Street’s most bullish outlook in Jan 2017 with a S&P 2700 target) released expectations for a recession by 2020 (morganstanlyFA.com) calling it “almost inevitable,” and still giving 2018 a 25% chance to enter a bear market. Thus, we continue to maintain that active management and meeting regularly with your advisor can help stay in front of a potentially looming bear market.

The new tax law should help provide fiscal support for the economy as monetary support is withdrawn. And although it helps decrease the chance of a recession in 2018 and even in 2019, market volatility may increase significantly from the extraordinarily low levels that persisted since 2015. The US Bonds market could potentially see its hardest year in a decades, and we continue to favor international as a more stable value appears present than domestic. Nevertheless, for markets and the economy, the new law appears to provide a firmer launching point as we enter the New Year.

Lastly, enclosed you will find LPL administered bullet points regarding the tax reform. We wish you a healthy and happy 2018. And as always, we encourage you to contact us with any questions.

Sincerely,

Your Friends at Maverick Wealth Management

Important Information

*Based on a trailing 12-month price-to-earnings ratio (PE) of 19–20. Forecasts are from our Outlook 2018: Return of the Business Cycle publication.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual security. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. Indexes are unmanaged and cannot be invested into directly.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

Economic forecasts set forth may not develop as predicted.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

The S&P 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

Investing in stock includes numerous specific risks including: the fluctuation of dividend, loss of principal and potential illiquidity of the investment in a falling market.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond and bond mutual fund values and yields will decline as interest rates rise and bonds are subject to availability and change in price.

This research material has been prepared by LPL Financial LLC.

Securities offered through LPL Financial LLC. Member FINRA/SIPC.

Tracking #1-681790 (Exp. 12/18)